Summary

- Second Dash for Gas pushed by government

- Idea totally disconnected from reality we face

- North Sea gas production in terminal decline

- UK gone from exporter to major importer

- Competition with Asia cutting LNG imports

- Imports from Europe unlikely to grow

- Consumption now being forced down

- Gas much more scarce and expensive

- Not the time to get even more addicted

- Establishment willing gamble on shale

- Because they will be insulated from costs

The plan for a new “Dash for Gas” announced by the government this week has been rightly denounced as bad for the climate, economy and environment. However there is another massive issue which no one is talking about. This is the fact that the whole idea is completely and utterly insane, when taken at face value. Though of course one has to be careful about labelling an idea insane, as it may be the case that a particular action makes complete sense when viewed with someones real motivations in mind. On the face of it though this new “Dash for Gas” has no connection to reality at all. The first “Dash for Gas”, which occurred in the 1990s, saw over 30 GW of generating capacity constructed, pushing gas from 5 percent to around 30 percent . At the time it was criticised as squandering gas since when used in homes it can produce heat at close to 100 percent efficiency whereas huge loses are involved in converting to electricity.

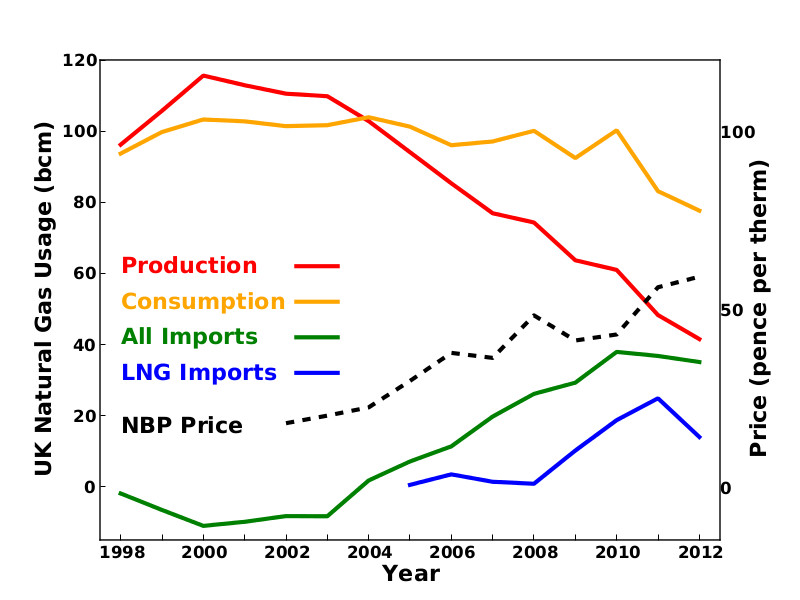

Regardless of your opinion on the merits of the first “Dash for Gas”, the position that the UK is in today could not be more different than that in 1990. Back then gas prices were low, North Sea gas production was rising quickly and it was easy for the establishment of the time to delude themselves that gas would be cheap and abundant forever. However gas production in the UK sector of the North Sea predictably peaked in 2000. Since 2003 gas production has been declining at a rate of around 7.2 bcm per year. If that rate of decline were to continue then UK North Sea gas production would fall to zero in around 6 years. In reality gas production is likely to tail off somewhat more gradually but first it must drop considerably in the coming years. The US Energy Information Administration (EIA) estimates that around 315 bcm of gas remains which would equate to 7 years at current production rates. It therefore seems clear that UK North Sea gas will not be playing a major part in UK supply past the end of this decade.

UK gas usage and price (dashed black line) over the last 14 years (data from DECC – 2012 values estimated from first 11 months)

On the imports front the situation is not a lot better. As gas production has declined, the UK has gone from a net exporter of gas (for a few years around peak gas production) to importing a significant amount of gas. In 8 years the UK gone from exporting gas to importing around 45 percent of its consumption, and this is only set to grow as production declines further. However it can be seen from the graph above that imports have risen to offset the drop in production and this is resulting in rising prices and falling consumption. The bulk of this imported gas comes from Norway, the Netherlands and Quatar, via liquified natural gas (LNG) tankers. Norwegian gas production is predicted to follow the UK into decline the next decade. In fact it may have already started with Norwegian gas production falling 4.6 percent between 2010 and 2011. Gas production in the Netherlands has been on a bumpy plateau for over a decade and must similarly decline at some point.

This only leaves more distant sources of imports to rely on for growth in gas imports. Here too the chances any increases look very slim. LNG imports from places like Quatar have risen quickly since they first became necessary in 2005, particularly since spot gas prices dropped following the recession. More recently however imports have nosedived this year due to competition from Asia for LNG cargoes. In October 80 percent lower than the same month in 2011 and total LNG imports for the year are likely to be down 50 percent on 2011. Even with much higher UK gas prices the chances of LNG imports increasing are not good. The majority of LNG is traded through long term contracts which are generally already locked up by Asian countries.

The only other potential source of gas imports is Russia but here again the outlook is bleak. Despite a lot of talk about Russian gas the UK does not import a great deal at present and there is little reason to believe huge increases are possible. Russian gas exports has been been flat for the last two decades and competition for them with Asia is growing. The Russian Economy Ministry has just revised down its projections of Russian gas production and exports by 6.8 percent this year and 4 percent next year. The UK sits right at the end of a long pipeline network stretching across Europe and is only likely to receive the leftovers at the highest prices. Despite talk of extending the Nord Stream (Russia-Germany) pipeline to the UK, the reality is that any increases in gas imports from Russia are going to be small and expensive.

When all this is stacked up against the desire of corporations and government to maintain business as usual it is not surprising that unconventional gas is seen as the only alternative. However to be a viable (if dangerous and destructive) alternative to North Sea gas, unconventional gas would actually have to be capable of significant production at affordable cost. The continued decline in UK gas production will open up a hole of several tens of bcm per year whether any new gas-fired power stations are built or not. Imports have risen but competition with other importers seems to be limiting further increases (unless prices rise significantly). This has already opened a hole of 20 bcm a year which has been solved by gas consumption dropping 20 percent in the last 2 years. In someways this gives the lie to the argument that we need the vast amounts of fossil fuels we use now in order to keep the lights on. There are plenty of potential savings that could be made in our still profligate energy usage, which do no involve plunging us all into darkness.

The problem is that under our present system, city fat-cats are still be able to spend tens of thousands of pounds a year keeping outdoor swimming pools heated to bath temperature through the winter while the poor are forced to turn off their heating to afford to eat. Sensible planned reduction of energy usage would run straight into these inequalities and cannot be countenanced by the establishment. In reality, institutions pushing the fantasy that fracking can bring a return to cheap and plentiful gas may well believe their own propaganda, but it is also true that if it doesn’t work out they aren’t going to be the people who suffer. We explored the large number of reasons why it is highly unlikely in a separate article (see Fracking Scam: Boom and Bust) and the effort and potential impacts involved in trying to produce this amount of unconventional gas in another (see Fracking Nightmare: Destroying Our Countryside). That the core of the government’s new energy policy is based around a set of brand new extraction techniques that have yet to produce any energy in the UK (and may never produce significant amounts) it is a clear indication of the desperation that exists in financial and political circles.